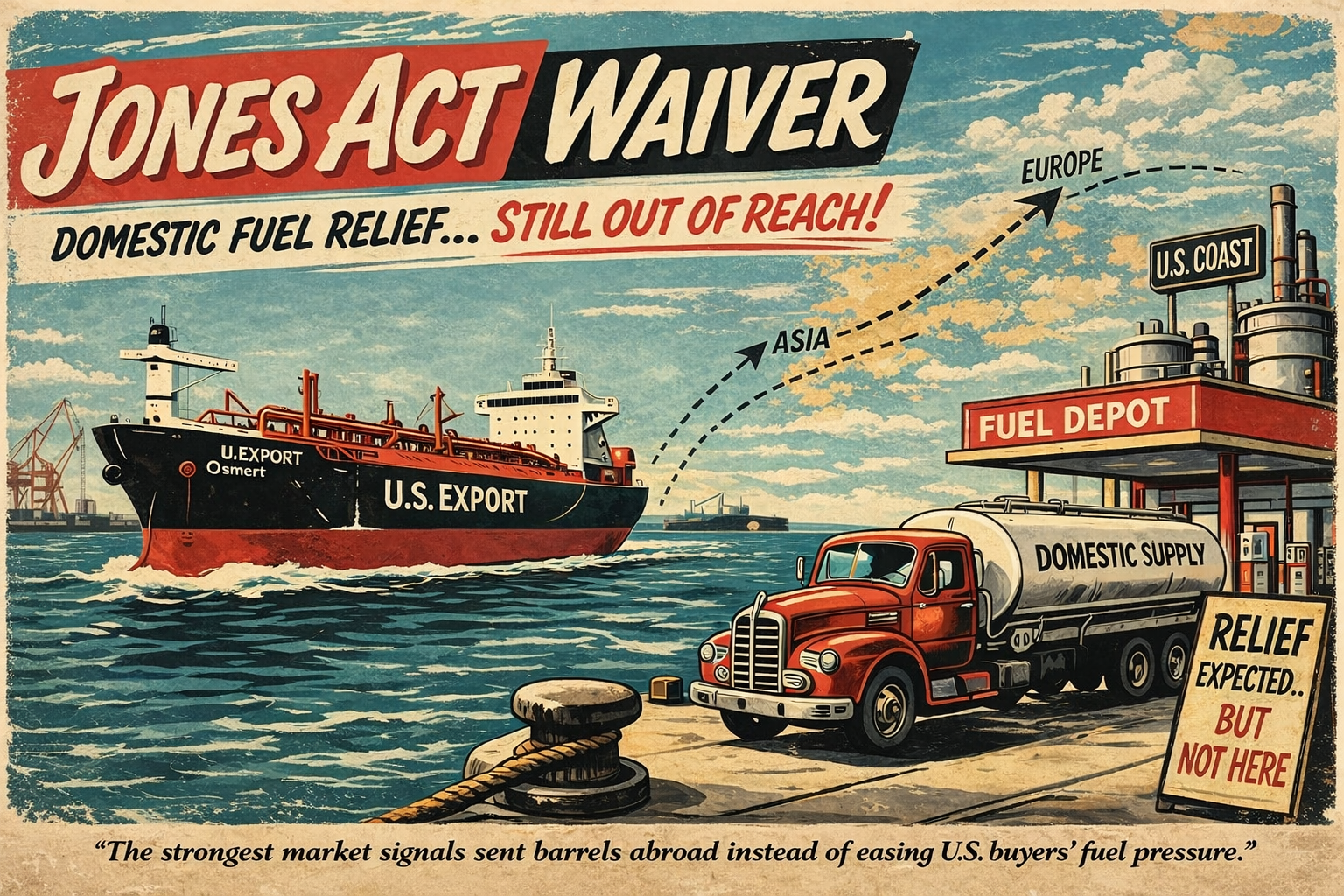

- The Jones Act waiver promised domestic fuel relief, but the strongest market signals sent barrels abroad instead.

- Record clean-product exports, tighter tanker availability, and weaker coastwise flows show how export arbitrage overwhelmed domestic shipping relief.

- New compliance guidance, falling distillate inventories, and rising freight pressure reveal why coastal buyers still have not seen the benefit many expected.

“Refinery output mattered, but the bigger story was where the barrels went after production — and too many of them went abroad.” (Refinery units and stacks at the Irving Oil Refinery in Saint John, New Brunswick.)

The Jones Act waiver was presented as a quick way to ease fuel pressure in the United States by allowing foreign-flagged vessels to move certain covered commodities between U.S. ports for 60 days. But the clearest market evidence now points in a different direction. The waiver remains in force through May 17, 2026. Yet, domestic coastwise liquid movements were essentially flat in March, while U.S. fuel exports surged to a record, showing that the legal flexibility existed. However, the commercial incentive still favored overseas markets.

There are also several important updates beyond the original waiver announcement. U.S. Customs and Border Protection updated its implementation guidance on March 27, clarified that covered cargo must be loaded onboard by the May 17 deadline, and attached an updated covered-products list. The Maritime Administration’s domestic shipping page now shows a new “April 8, 2026 – 9:00 am – MARAD 501c Waiver Report” entry under the March 17, 2026 waiver, indicating that the reporting phase is no longer theoretical. At the same time, fresh EIA-linked reporting on April 8 showed U.S. distillate inventories falling by 3.1 million barrels while distillate exports rose to 1.58 million barrels per day, even as ceasefire hopes pushed crude futures sharply lower.

Taken together, those developments keep the pressure squarely on refiners, traders, shippers, carriers, terminals, and agricultural buyers. The relevant products are not just generic “oil.” The market segments now showing the most strain include crude oil, gasoline, diesel, naphtha, jet fuel, petrochemicals, biofuels, liquid chemicals, and fertilizer-related cargoes. Reuters, AFPM, and the American Farm Bureau Federation all describe the waiver’s practical relevance in those terms, which means the story reaches well beyond Washington and into the day-to-day realities of fuel supply, vessel availability, and downstream pricing.

For related background on how petroleum, sanctions, and maritime chokepoints intersect with U.S. strategy, read our Iran oil and gas history of U.S. strategy.

Why has the Jones Act waiver not lowered domestic fuel pressure?

“The waiver landed in a market already shaped by a global chokepoint shock, and that shock kept export demand elevated.” (EIA graphic showing petroleum flows through the Strait of Hormuz.)

The short answer is that the Jones Act waiver changed legal access to ships, but it did not change the strongest price signals in the market. March data show that crude oil, refined products, biofuels, and liquid chemicals shipments between U.S. ports held roughly steady at about 1.37 million barrels per day from February to March, while Gulf Coast liquids exports to other U.S. coastal markets actually fell to 770,000 barrels per day from 826,000 barrels per day. Over the same period, U.S. clean-product exports jumped to a record 3.11 million barrels per day. That gap is the heart of the story.

For domestic buyers, that matters more than the symbolism of the waiver itself. California, Hawaii, and marine-dependent coastal markets were part of the political logic behind the move because low availability of U.S.-flagged vessels has long been blamed for limiting Gulf Coast-to-coast deliveries. But a waiver can only widen the menu of vessels. It cannot force refiners, traders, or shipowners to choose a lower-paying domestic voyage over a richer export run to Europe or Asia. As long as export arbitrage remains stronger, the Jones Act waiver is more likely to alter options on paper than outcomes at the rack or terminal.

For more freight, regulation, and market movement across the sector, browse our transportation industry coverage.

What did the Jones Act waiver actually change in March 2026?

At the legal level, the Jones Act waiver temporarily carved out an exception to a coastwise shipping law that normally requires merchandise moved between U.S. points to travel on U.S.-built, U.S.-owned, and coastwise-endorsed vessels. MARAD’s current domestic shipping page also emphasizes that waivers are tied to national-defense authority under 46 U.S.C. § 501, not normal commercial convenience, which is why waivers are comparatively rare and why they attract so much attention when they appear.

For more on rule changes, enforcement, and compliance impacts across tank transport, see our regulations and compliance coverage.

This specific Jones Act waiver was issued by the Department of Homeland Security on March 17, 2026, under 46 U.S.C. § 501(a), at the request of the Department of War, and CBP’s implementation notice says it expires at 11:59 pm EDT on Sunday, May 17, 2026. That procedural point matters. MARAD explains that a defense-route waiver under Section 501(a) can be granted immediately on national-defense grounds. In contrast, a separate civilian-route process under Section 501(b) involves a non-availability determination for coastwise-qualified U.S. vessels. AWO underscored the same distinction when it argued that this 2026 action did not involve a survey of available domestic vessel capacity.

Public descriptions of the covered cargoes also show why the waiver drew such broad attention. Reuters reported that the White House framed the action around oil, natural gas, fertilizer, coal, and other energy-related cargoes. At the same time, later trade-group and legal analyses pointed to crude oil, refined products, petrochemicals, and other HTS-coded commodities on the list. Legal practitioners described the original March 18 attachment as containing 659 potentially covered products, and CBP later circulated an updated list dated March 27.

How did CBP tighten Jones Act waiver compliance on March 27?

“Geography shaped the market before the waiver ever did, because disruptions around Hormuz changed the value of every available barrel.” (Map showing the Strait of Hormuz in relation to Iran, Oman, and the Arabian Peninsula.)

The March 27 CBP update is one of the most important fresh developments because it moved the story from a broad announcement into operational rulemaking. CBP said the updated guidance included a revised covered-products attachment and clarified that, to be compliant, any covered product must be loaded onboard the vessel before the waiver expires at 11:59 pm EDT on May 17. That is more precise than a vague “60-day window” and gives shippers, charterers, and editors a concrete deadline with real commercial consequences.

CBP’s notice also laid out the paperwork in unusually practical terms. Trade participants using the Jones Act waiver are asked to notify CBP with the vessel name, IMO number, flag, commodity and HTS code, carrier, and ports and dates of departure and arrival. Foreign-flagged vessels moving cargo under the waiver still must comply with vessel entrance and clearance rules, use VECS in ACE, and provide a paper CBP Form 1302 for domestic cargo. CBP even specified the exact wording for domestic shipments that should be included on the form, which is the kind of compliance detail industry readers actually need.

For a closer look at fuel-rule changes affecting fleets and documentation, read our HM-265 fuel compliance guide.

The post-voyage side matters too. CBP reiterated that, under 46 U.S.C. § 501(c), vessel owners or operators and requesters must report voyage details to MARAD no later than 10 days after the voyage ends, including vessel identity, dates, ports, cargo description, and the explanation for the national-defense interest. MARAD’s page now shows a current April 8 waiver-report entry under the March 17, 2026 waiver heading, which strongly suggests the public reporting stage has begun and that at least one voyage under the Jones Act waiver has moved far enough through the system to trigger publication.

Which Jones Act waiver products and routes are really in play?

For practical purposes, the most important cargoes under the Jones Act waiver are the ones tied to fuel availability, refinery economics, industrial feedstocks, and farm input costs. Reuters and trade-group responses point to oil, natural gas, coal, fertilizer, crude oil, refined products, and petrochemicals. Reuters’ shipping data also show that the domestic market categories under watch include crude, refined products, biofuels, and liquid chemicals. At the same time, its export reporting highlights gasoline, naphtha, diesel, and jet fuel as the clean-product streams now moving aggressively into overseas markets.

For more on crude hauling, export pressure, and market shifts, browse our crude oil coverage.

The route question is almost as important as the product question. The public CBP bulletin does not spell out narrow geographic caps inside the text, and legal observers have said the guidance appears broad enough to cover trade between U.S. points, including non-contiguous markets such as Alaska and Hawaii, so long as the commodity is on the covered list and the compliance conditions are met. That interpretation makes the Jones Act waiver more commercially significant than a narrow disaster-only carveout, because it means the waiver was theoretically relevant to West Coast, island, Gulf Coast, and East Coast supply chains all at once.

But theoretical breadth is not the same as actual uptake. The key point is that route eligibility did not solve the margin problem. Even if the Jones Act waiver widened the range of possible domestic lanes, the most lucrative lanes in late March and early April were still the export lanes. The real issue is not just what could move, but what actually moved.

Why are export economics overwhelming the Jones Act waiver at home?

“The waiver expanded access to ships on paper, but export economics still steered product toward higher-paying overseas routes.” (The oil products tanker BRO NISSUM underway in daylight.)

The clearest evidence comes from the March export data. Reuters reported that U.S. exports of clean petroleum products rose to about 3.11 million barrels per day in March from about 2.5 million barrels per day in February, the highest monthly level in Kpler’s records dating back to 2017. Exports to Europe climbed 27% to 414,000 barrels per day, exports to Asia more than doubled to 224,000 barrels per day, and exports to Africa jumped 169% to 148,000 barrels per day. Reuters also flagged unusual flows from the U.S. Gulf Coast to Australia and about 72,000 barrels per day from the U.S. East Coast to Europe, even though the East Coast normally imports diesel from Europe.

For a closer look at how Gulf disruption is pressuring tanker rates, diesel prices, and fleet planning, see our Hormuz shock reporting for oil transportation fleets.

Those barrels moved because the international shortage was enormous. S&P Global reported that more than half of the world’s refining system was exposed to the Middle East conflict, either directly or through crude supplies tied to the Strait of Hormuz. In contrast, more than 4 million barrels per day of refined-product exports through Hormuz had been completely halted. In that context, the Jones Act waiver did not create a new export incentive; it landed in a market that was already paying aggressively for replacement barrels.

Pricing confirms the same logic. Reuters reported on April 6 that European gasoil futures were trading above $200 a barrel while U.S. ultra-low sulfur diesel futures were under $185. The same day, Reuters also reported that WTI Midland premiums delivered to North Asia had jumped to roughly $30 to $40 a barrel above benchmark pricing. In comparison, WTI Midland delivered into Europe was near a record premium of about $15 a barrel over dated Brent. When those are the economics, the Jones Act waiver cannot by itself redirect enough tonnage back into domestic coastal circulation to change the broader narrative.

That is also why tanker availability tightened instead of loosening. Reuters said shipowners were making more on longer-haul export voyages, and S&P Global said stronger U.S. refined-product exports, plus legislative shifts in the United States, absorbed more tonnage and pushed clean-tanker markets to multiyear highs. The waiver may have increased flexibility, but export arbitrage still decided where the ships and cargoes wanted to go.

For more on tanker markets, marine logistics, and rate-sensitive vessel movements, explore our tankers coverage.

Where is the Jones Act waiver showing up in prices, inventories, and tanker rates?

The domestic flow numbers remain the most damaging data point for the policy case. Reuters reported that shipments of crude oil, refined products, biofuels, and liquid chemicals between U.S. ports were virtually unchanged in March from February at about 1.37 million barrels per day. More tellingly, liquid exports from the U.S. Gulf Coast to other U.S. coastal markets fell to 770,000 barrels per day from 826,000 barrels per day. So the Jones Act waiver did not produce a visible surge in coastwise energy traffic in March.

“Tighter distillate balances and stronger exports meant the promised domestic relief still did not show up where buyers feel it most.”

Freight data show why. S&P Global said clean tanker rates for a 38,000-metric-ton cargo from the U.S. Gulf Coast to the U.K./Continent route were assessed at $95.12 per metric ton on March 27 after reaching $124.21 per metric ton on March 24, which was 185% above the five-year average. S&P also said U.S. exports of refined products to Northwest Europe rose to 429,200 barrels per day in March, above the 2025 average of 371,400 barrels per day, and described the traditional relationship between U.S. Gulf-to-Europe and Europe-to-U.S. Atlantic Coast routes as having effectively reversed. In plain language, the trans-Atlantic trade became so strong that it began to function as the front-haul market.

EIA-linked reporting on April 8 added another layer. Reuters said U.S. distillate stocks fell by 3.1 million barrels to 114.7 million barrels in the week ended April 3, while distillate exports rose to 1.58 million barrels per day. Gasoline stocks also fell by 1.6 million barrels. Crude inventories rose, but that did not erase the tighter product balance. For anyone covering diesel, freight, or industrial fuel users, this is the key nuance: crude can build while refined-product markets still feel tight, and that is exactly the kind of backdrop in which the Jones Act waiver struggles to deliver immediate domestic relief.

For more petroleum balances, refinery utilization trends, and federal energy data, explore our EIA reports and market data coverage.

The macro backdrop is still unstable as well. Reuters analysis on April 8 said that crude futures plunged on hopes of a ceasefire. However, physical crude and refined-product markets remain stressed because supply-chain damage from the effective closure of Hormuz is still moving through the system. The same analysis highlighted Saudi Aramco’s substantially higher May official selling prices and argued that wealthy buyers may continue to outbid poorer regions for available supply. That matters for the Jones Act waiver because domestic relief is harder to achieve when the world is still competing for every marginal barrel.

What does the Jones Act waiver mean for California, Hawaii, and East Coast buyers?

“Domestic fuel supply did not get the lift many expected, as higher-paying export markets continued to outbid U.S. coastal demand.”

California and Hawaii remain central to the political and editorial case for the Jones Act waiver because Reuters explicitly noted that low availability of Jones Act-qualified vessels was partly blamed for high fuel prices in California, Hawaii, and other U.S. markets without pipeline links to Gulf Coast refiners. Those are the places where a marine workaround sounds most attractive in theory. In practice, however, the export pull has been stronger than the domestic pull.

That pressure is still visible in retail pricing. EIA’s April 7 gasoline and diesel update showed U.S. regular gasoline averaging $4.12 per gallon and on-highway diesel averaging $5.643. On the West Coast, gasoline averaged $5.396 and diesel $6.924, while California alone was at $5.769 for gasoline and $7.567 for diesel. The East Coast, by comparison, averaged $4.00 for gasoline and $5.740 for diesel. Those numbers do not prove that marine shipping alone caused the gap. Still, they underscore why coastal and non-contiguous markets remain so sensitive to tanker availability, replacement costs, and unexpected export competition.

For additional reporting on diesel supply, pricing, and downstream pressure, visit our diesel fuel news coverage.

The East Coast adds one more telling wrinkle. Reuters said about 72,000 barrels per day of clean products moved from the U.S. East Coast to Europe in March, the second-highest level in Kpler’s records, even though the region usually imports diesel from Europe. S&P Global also said the Jones Act waiver should, in theory, divert some export barrels to the West Coast and PADD 1, but firm evidence of that impact had not yet emerged by late March. That combination captures the moment clearly: domestic diversion is still a theory; the export draw is already a fact.

What should carriers, terminal operators, and fuel haulers watch before the Jones Act waiver expires?

The first date to watch is May 17, but not in a vague way. Under CBP’s March 27 clarification, the relevant compliance trigger is whether the covered product is loaded onboard before 11:59 pm EDT on May 17. That means chartering decisions, terminal windows, customs coordination, and cargo sequencing all matter right up to the deadline. The second thing to watch is MARAD’s public reporting page. Now that the page shows an April 8 waiver-report entry, industry readers should expect more visibility into actual usage patterns if additional voyages are reported under Section 501(c).

The third variable is the export market itself. If the ceasefire proves durable and Hormuz traffic normalizes, export arbitrage could soften, tanker availability could improve, and the Jones Act waiver might yet matter more in the back half of its life than it did in March. But if physical shortages persist, if Atlantic Basin freight stays elevated, or if distillate exports remain strong, domestic relief may continue to underperform expectations even with the waiver still active. That is not a legal failure. It is a market outcome.

The stakeholder split is also worth watching because it tells readers where the next political fight may go. AFPM welcomed the added flexibility around crude oil, refined products, and petrochemicals. The American Farm Bureau Federation applauded the move as a way to get more ships carrying critical fuel and fertilizer materials during spring planting. On the other side, AWO said the waiver would inject international price volatility into domestic commerce and have no appreciable effect on gasoline. At the same time, the AFL-CIO called it unnecessary and ineffective. Those reactions matter because the Jones Act waiver is now both a shipping-market story and a broader argument about industrial policy, labor, and energy security.

The bottom line is this: the Jones Act waiver did not fail because no one understood the rules. The rules are now clearer than they were on day one, the product list has been updated, the loading deadline has been defined, and MARAD’s reporting track appears to be active. What failed to materialize was the hoped-for domestic flow response. The barrels moved, but too many of them moved toward higher-paying export markets rather than into U.S. coastal relief lanes.

For related reporting on fuel-market pressure, refining disruptions, and downstream impacts, see our fuel industry coverage.

For industry readers, that leaves a very practical conclusion. The next two questions are not “what is the Jones Act?” or even “is the waiver still in effect?” The sharper questions are whether freight remains too expensive for domestic redistribution, whether distillate balances continue to tighten, whether West Coast and East Coast buyers see any real coastal diversion, and whether more publicly posted waiver reports begin to show how the exemption is being used in the field. Until those answers change, the Jones Act waiver is best understood as a measure that expanded legal flexibility but did not yet overcome global price signals.

What the Jones Act waiver changed — and what it didn’t

Key Developments

- The Jones Act waiver remains active through May 17, 2026, but domestic fuel relief has been limited in practice.

- CBP updated its guidance on March 27 and clarified that covered cargo must be loaded onboard before the waiver expires.

- Domestic shipments of crude oil, refined products, biofuels, and liquid chemicals between U.S. ports stayed broadly flat in March.

- Gulf Coast liquids flows to other U.S. coastal markets declined instead of rising under the waiver period.

- U.S. clean-product exports surged to record levels, pulling more barrels toward Europe, Asia, and Africa.

- Stronger overseas margins made export routes more attractive than domestic coastwise moves.

- Tanker availability tightened as longer-haul export voyages absorbed tonnage and pushed freight rates higher.

- Distillate inventories fell while exports climbed, reinforcing the pressure on domestic fuel markets.

- California, Hawaii, and other marine-dependent markets remain exposed to high replacement costs and constrained vessel availability.

- The core takeaway is that the Jones Act waiver expanded legal flexibility, but it has not yet overcome global price signals.

Jones Act Waiver: External Sources, Market Data, and Industry Response

- Review CBP’s implementation guidance and the March 27 Jones Act waiver update.

- Understand MARAD’s domestic shipping framework and Jones Act waiver authority.

- Track the latest EIA gasoline and diesel retail price update

- See EIA’s analysis of first-quarter 2026 crude oil and petroleum product price spikes

- Read AFPM’s response to the temporary Jones Act waiver and its implications for fuels and petrochemicals

- See how the American Farm Bureau Federation framed the waiver for fuel and fertilizer supply needs

- Read the American Waterways Operators’ statement opposing the broad 60-day Jones Act waiver

- Follow Reuters’ report on the original Jones Act waiver announcement and policy intent

- Review Reuters’ reporting on record March fuel exports and overseas demand pull

- Read Reuters’ analysis of why the Jones Act waiver did not materially boost domestic oil flows

- See Reuters’ summary of EIA inventory data showing falling gasoline and distillate stocks

- Explore Reuters’ reporting on why physical oil markets remained stressed despite ceasefire hopes

- Examine S&P Global’s reporting on trans-Atlantic clean tanker rates and export-driven freight pressure